Harshad Shantilal Mehta, also known as the ‘Big Bull’ and ‘Amitabh Bachchan’ of the Indian stock market was a stockbroker, responsible for the biggest financial scam ever witnessed in India. To put things in perspective, the scam orchestrated by the big bull, Harshad Mehta was:

- Larger than the health and education budget of the entire country.

- 50 times the size of the Bofors’ scam.

- The BSE witnessed a 12.77% fall in one day, the biggest fall in BSE’s history.

- Rs 10,000 crores worth of market capitalisation was wiped off in a single day.

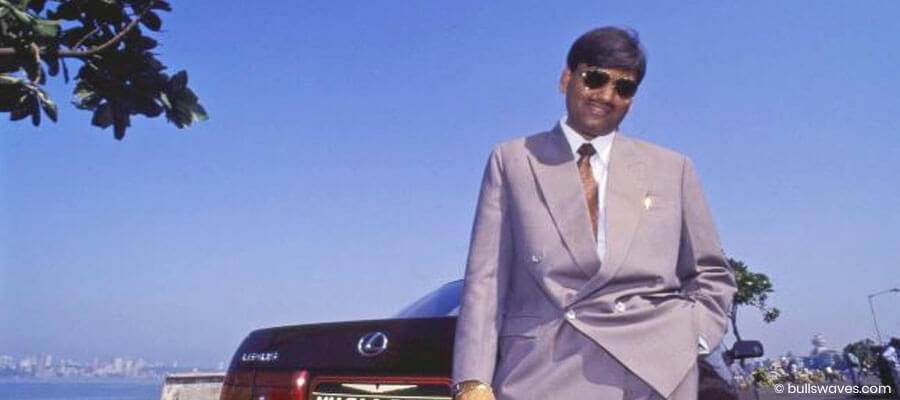

The story of Harshad Mehta, the evergreen big bull of the Indian stock market is nothing short of a fairytale gone wrong. From a 1 room apartment in a ghatkopar chawl to a 15,000 sq-ft sea facing apartment in Worli, with a swimming pool and a golf course to the collection of imported cars, including the Toyota Lexus worth Rs. 45 lakhs in 1992, to a lonesome death in Thane jail, the rise and fall of the big bull, Mr Harshad Shantilal Mehta has been catastrophic.

From a stock market jobber to the ultimate big bull, Harshad Mehta single-handedly transformed the fate of the Indian stock markets and the country.

Today, we look at the man behind the name, the deals behind the scam and the big bull behind the biggest financial scam in India - the 1992 securities scam, also known as the ‘Harshad Mehta Scam’.

Early Life – From a salesman to the best jobber

Born on 29th July 1954 at Paneli Moti, Rajkot, to Shantilal Mehta, (a small textile trader) and Rasilaben Mehta, Harshad Shantilal Mehta was the youngest of the two sons. The Mehta’s resided in Kandivali in Mumbai and later shifted to Mouda Para in Raipur, Madhya Pradesh. Post his schooling, he shifted back to Mumbai and completed his B.Com from Lala Lajpat Rai College in 1976.

Post his graduation, he worked odd jobs as a hosiery, cement salesman and a diamond sorter. He then joined New India Assurance Company Ltd as a salesman. During his stint at the New India Assurance Company Ltd, he got interested in the stock market and soon resigned from his job to join a broking firm.

In the early 1980s, he worked as a Jobber under Prasann Pranjivandas Broker, who he considered as his guru. Within a year, he became one of the best jobbers in the Indian stock market.

But discontent with the meagre commission that jobbers made, he decided to become a stockbroker with BSE himself and opened his own stock advisory firm, ‘GrowMore Research and Asset Management’ with his brother Ashwin Mehta. Many prominent and effluent people started investing with his firm and Harshad Mehta soon became the unofficial poster boy of the Indian stock market.

With a huge capital base, Harshad started manipulating the stock prices of stocks recommended by GrowMore Research and Asset Management. One of his favourite stocks was Associated Cement Company (ACC). Harshad blindly pumped money into ACC, raising its stock price from Rs 200/share to Rs 9,000/share in just 3 months; an increase of 4,400%!

Any whispers of price manipulations were shut down by his self defined ‘replacement cost theory’. He simply argued that the company was undervalued and its fair value should be decided by the cost required to build a similar company in the current times. While flawed, due to his charisma and authority in the stock market, no one questioned the big bull and Harshad continued manipulating the stock prices.

His ‘research’ was simple; He handpicked a company and then spread rumours of the company’s huge growth prospects. He then recommended all his clients to invest in the selected stock and once the rumours spread, other investors would also pump money into the stock and drive up its prices. Once the prices were up, he would sell his stocks and book his profits.

Harshad Mehta, arguably, spearheaded the bull market run in 1991, which aptly made him the ‘big bull’ of the Indian stock markets. In the same year, he was one of the highest advance tax payers in the country, having paid an advance tax of Rs 26 Crores!

While this method worked and Harshad made a lot of money, he knew that driving up the market would require enormous capital; capital that was free flowing in the Indian money market.

Prelude: The Indian Money Market of the 1980s

The Indian money market was a marketplace where bonds, treasury bills and other fixed income instruments issued by the RBI traded. At its core, the structure was simple: One bank wanting to sell securities to another bank would hire a broker to facilitate the exchange for a small commission.

But the Indian money market was shallow and dominated by five players only - The leader, Citibank and the big brokers, DSP, VBD, C Mackertich and BCD (owned by Bhupen Dalal).

Between 1987-1992, money market brokers underwent a huge transformation. With foreign degrees and technology, they started emulating the foreign banks like Citibank. Brokers like Harshad Mehta, his brother Ashwin Mehta had the expertise, knowledge and understanding that surpassed these banks and soon the non-trading banks started looking like passive brokers.

In a couple of years, money market brokers surpassed the trading volume of the money market mafias. The role of brokers witnessed a massive growth as the Narasimha Rao government moved towards a system driven by markets and not government diktats. This meant that institutions such as IDBI, ICICI etc. who were fed easy money would now be required to raise their own capital from the market with the help of brokers. All of a sudden, brokers like Harshad Mehta had become the key players in the Indian money market.

First Act: Banks forced to invest in high-risk bonds

The 1992 Harshad Mehta Scam was inevitable. The scam was a result of over two decades of over-regulation on paper, lack of regulation in practice, misguided RBI policies and a creaky financial infrastructure.

After the liberalisation of the Indian economy in 1991, the government pressured Indian banks to compete and earn profits as they were close to bankruptcy. But competing with foreign banks and their advanced technology was an uphill struggle, especially since the banks had little freedom and capital for investments.

Till the 1992-93 budget, banks were forced to maintain 38.5% of their deposits as a statutory liquidity ratio (SLR) in low-interest bonds issued by the government and its entities. Another 25% was forced to be maintained as a cash reserve ratio (CRR) in treasury bills. These low-interest bonds financed the government’s ever-increasing appetite for cash.Even with the remaining 36.5% ‘free’ capital, the banks were forced to focus on priority sector and political lending.

This meant that the banks had to dabble in high-risk-high-return bonds issued by other banks to improve their bottom line. Thus, the banks started approaching brokers like Harshad Mehta, to find and execute high return bond deals for them, setting in motion the 1992: Harshad Mehta scam.

Second Act: A unique ready forward deal (RFD)

Apart from the SLR and CRR roadblocks, Indian banks were also not allowed to invest in the stock market. So, their entire quest for improving their bottom line was heavily dependent on brokers like Harshad Mehta securing top deals for them.

The Indian banking sector was a jungle with the State Bank of India (SBI) as the dominant player residing with other small sized banks. These small-sized banks often faced temporary SLR and CRR deficits and would borrow from big banks and institutions to avoid being penalised by the RBI.

Before we reveal the second act, it is important to understand the banking system of the 1980s - 1990s. This was an era, where all the records were maintained physically in government offices. There were no digital records. The RBI had a Public Debt Office (PDO), which maintained the records of all the securities issued and transactions between the banks. The records were reconciled by each bank against the PDO records every quarter.

The banks would buy and sell securities through a Ready Forward Deal (RFD). A RFD is a secured short-term loan of 15 days against a collateral. These RFDs were secured against government bonds.

While on paper the securities were bought and sold, in reality, when banks buy or sell government securities they rarely exchange papers. They exchange Subsidiary General Ledger (SGL) notes. SGL was issued as a substitute to exchanging actual securities. But often, Bank Receipts (BR) would be used instead of SGL Notes.

A bank receipt was issued by banks who sold the securities but were unable to make immediate deliveries. They specified what had been sold and that funds were received from the lending bank while the securities would be delivered on a later date. Once the delivery was made, the bank receipts stood discharged.

So, a bank receipt would confirm that the borrowing bank will deliver the securities at a later date. This assured the lending bank that the bank receipts were issued against a collateral.

Also the settlement cycle was 14 days. So, if SBI loans money to PNB against a BR, then PNB has to deliver the securities within 14 days.

Brokers like Harshad Mehta, were the middlemen of the ready forward deals. Ideally, the lending bank would issue the cheque in the name of the borrowing bank, but Harshad Mehta would promise banks a higher rate of return in exchange for transferring the funds in his personal account. He termed this as making them ‘bank-rich’. So, cheques worth crores of rupees would be made out to Harshad Mehta instead of PNB or other banks.

Harshad Mehta would deposit these cheques and since the settlement cycle was 14 days i.e. he had to pay the borrowing bank only after 14 days, so for 14 days Harshad Mehta owned crores of rupees.

He diverted these crores to rupees to the Indian stock market especially rigging the stock prices of his favourite stocks, ACC, Videocon, Sterlite Industries etc and taking the BSE to new heights. He single-handedly tackled all the market bears like Rakesh Jhunjhunwala, Manu Mundra and others, who had short the market, in absence of any fundamental factors driving the market rally.

With an inflow of crores of rupees, the stock prices rose drastically, enticing other investors to invest in the script. As and when investors flocked to these scripts (nearing the end of the 14-day settlement cycle), Harshad would sell his investments, pay the loan amount to the borrowing bank as mentioned in the BR, and deliver the securities to the lending bank.

The game was simple. Everything was squared off after 14 days. The lending bank got the securities, the borrowing bank got the capital, and Harshad made money in the market.

In a normal ready forward deal, only two banks were involved. But the brilliance that is Harshad Mehta, involved multiple banks. He would get the money from Bank A and ask for 14 days to deliver the securities. Consecutively, he would get the securities from Bank B and ask for 14 days to deliver the funds.

For these 14 days he invested the funds in the stock market. After 14 days, he simply had to liquidate his position from the market and pay the funds to Bank B. But what happens when the markets tank and Harshad cannot liquidate his position?

He would then approach Bank C, and get the securities from them and deliver to Bank A and ask for another 14 days to deliver the cash to Bank C. This went on for a while and by the end of it all, Harshad Mehta had ‘officially’ transferred crores of rupees from the Indian money market to the Indian stock market. Banks were unintentionally a party to the Indian stock market.

Third Act: Issuance of fake bank receipts

Remember, brokers were intermediaries in a RFD where lending and borrowing banks remained anonymous. They only knew the broker and an SGL note or a BR was proof enough for them to issue cheques in the name of the broker. And if that broker was the biggest name in the stock market, Mr Harshad Mehta, then no one batted an eyelid while issuing cheques worth crores of rupees.

UCO bank issued 50 crores to Harshad Mehta in clean credit i.e. without any collateral. The biggest bank in India, the State Bank of India, issued him Rs 500 crores on the basis of unverified bank receipts. This trust and his name was the catalyst in the 1992 Harshad Mehta scam. But Harshad soon realised that he would run short of banks to get the bank receipts from. That is when he decided to print fake bank receipts.

He convinced small sized banks - Bank of Karad (BOK) and Metropolitan Co-operative Bank (MCB) to issue him fake bank receipts, guaranteeing to make them ‘bank-rich’. These bank receipts were just pieces of paper without any collateral. A collateral guaranteed that if the borrowing bank could not repay the lending bank after the agreed period, then the lending bank would take the bank receipts to the PDO and get the securities transferred in their name. Only in this case, there would be no corresponding records with the PDO because the bank receipts were fake.

The climax: The discovery of the Rs 500 Crore SBI ‘loot’

In March 1992, CL Khemani, deputy managing director, treasury and investment management at SBI told RL Kamat, the deputy general manager, to start reconciliation work so that SBI’s books balanced with the PDO records as on 31st March 1992.

The records were maintained by R. Sitaraman, a junior management grade officer, who later emerged as a key figure in the 1992 Harshad Mehta scam. After the reconciliation, there was a difference of 74 crores between SBI books and PDO records. Khemani became suspicious and asked the assistant manager to get the original records from the PDO.

On 11th April 1992, SBI’s balance of the 11.5% central loan of 2010 maturity was 1170.95 crores whereas someone had altered the PDO statement so that Rs 1170.95 crores read as Rs 1,670.95 crores. Someone had looted the biggest bank in the country, the banker to the government worth Rs 500 crores.

After the questioning of R Sitaraman, it was revealed that the mastermind behind the Rs 500 crore loot was none other than the big bull,Harshad Mehta. Harshad Mehta was immediately called in the SBI branch and was asked to pay the bank or deliver the securities.

The market was down and therefore he couldn't sell his shares and pay back the money. Also the bank receipts issued to the SBI were fake, so they had no underlying securities.

The rumours of Harshad Mehta’s constant presence and the ongoing enquiry at SBI headquarters soon reached the inquisitive eyes of many journalists, including the very own Ms Sucheta Dalal.

The Final Act: Rs 4000 crore scam exposed

Sucheta Dalal, a journalist at the Times of India, was intrigued by the wealth and luxurious lifestyle of a common stock market broker. His fleet of cars, a mini in-house golf course was a rarity even for the rich. What was even more intriguing was how a stock market broker could have a networth of Rs 3000 crores in 1992. As she delved deep into the source of his networth, she uncovered just how Mr Mehta was looting the Indian banks and diverting the funds to the Indian stock market to inflate the stock prices.

On 23rd April 1992, Ms Sucheta Dalal published a full expose on Harshad Mehta, which shocked the entire country. The bankers were scrambling to verify their bank receipts and the Indian stock markets crashed from 4,467 to 2,000, wiping out 10,000 crores of market capitalisation in a single day.

This stock market crash was discussed extensively in the parliament and a CBI enquiry, headed by K. Madhavan was initiated to unearth the entire fraud. The RBI was also conducting an internal audit of the banks and soon uncovered fake bank receipt fraud of a whopping Rs 4,000 crores - The biggest financial scam ever witnessed by independent India.

After the entire fraud was discovered, Harshad Mehta was charged with 72 criminal offences and more than 600 civil suits were filed against him. The RBI also constituted the Janakiraman committee to investigate the fraud and the quantum of the fraud was said to be Rs 4,025 crores.

On 9th November 1992, Harshad and his brother Ashwin Mehta were arrested by the CBI for misappropriating more than 28 Lakh shares worth Rs 300 crores through forged share transfer forms.

After 3 rigorous months in Jail, Harshad Mehta did make a small comeback as a stock market guru, giving stock market tips and advice via his website. But in September 1999, the Bombay High Court sentenced him to five years of imprisonment and a fine of Rs 25,000. He was also barred from the Indian stock market for life.

Post an inquiry into his sources of income, the Income Tax Department charged Harshad Mehta and his wife, Jyoti Mehta with a tax evasion notice of Rs 11,174 crores.

The curtain close: Conviction and imprisonment

After being convicted by the Bombay High Court, Harshad Mehta was imprisoned in the Thane prison. On the eve of 31st December 2001, as the world welcomed the new year, Harshad Mehta suffered a cardiac arrest and breathed his last breath at the age of 48. He was survived by his wife and son, Atur Harshad Mehta.

A total of 27 cases are still pending against Harshad Mehta. His brother, Ashwin Mehta, became a lawyer and represents the family in court.

End Credits

A stock market guru to many, a fraud and con artist to most, Harshad Mehta was the original-ever-optimistic big bull of the Indian stock market. Many argue that he simply exploited the loopholes in the already crooked Indian banking system, but the truth is that he did use fake bank receipts to dupe Indian banks worth crores of rupees.

The 1992 Harshad Mehta scam could have been prevented by banks (by not issuing cheques in broker’s name) or the RBI (proper audit of the banks) or even Harshad Mehta himself (by just being a broker in the Indian money markets), but the magic of high-return-in-short-term entices us all. We all want that 4,400% return in 3 months.

Sentiments are every investor’s doom. Not every stock listed in the market is worth your time and money. Off the 5000+stocks listed on the exchange, barring 2-3% good stocks, rest of the stocks are sentiment driven. There is a Harshad Mehta on every corner in the stock market, with his own unique replacement cost theory, trying to sell you a stock that will make him rich and you poor.

So, before you get all excited and invest in a stock because it's the next Reliance or Infosys, explore StockBasket - India’s first long-term buy and hold investment platform, which caters to all your financial goals with quality, handpicked expert-curated stocks.

At StockBasket, our goal is to become your Warren Buffett not Harshad Mehta.