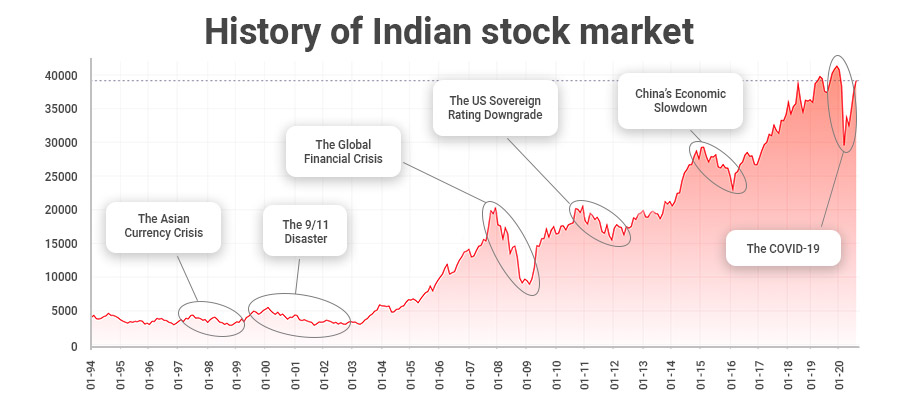

The Asian Currency Crisis (1997), the 9/11 disaster (2001), the Global Financial Crisis (2008), the US Sovereign Rating Downgrade (2011), China’s Economic Slowdown (2015), and the COVID-19 (2020), the stock market has suffered a lot of bruises from such massive body blows, but it has continued its mercurial rise.

Such an exemplary performance is characterised by the SENSEX, which has multiplied nearly 10 times since its inception. SENSEX is a stock market index comprising 30 well-established and financially sound companies listed on the Bombay Stock Exchange.

Looking back in history, while the stock market may seem volatile in a short time, it has a massive potential to generate a vast corpus of long-term wealth. The economy may go through an extended period of slump, but robust companies with strong fundamentals survive while antifragile companies grow, thrive and feed on such transient economic challenges. And looking back, compared to the tottering and galloping bull runs, the length of the bear runs have been tiny and minuscule.

Just to provide an overview of the massive rise in the stock markets, Rs 1 lakh invested in SENSEX in 1984 would be Rs 1 crore in 2017.

Types of investments

Let us address the elephant in the room “Long-term investments” by classifying the investments based on a specific term. Long-term investments, medium-term investments, and short-term investments are used interchangeably due to the relativity of time, as some investors consider even 1 year to be long-term investments. Based on the standard definitions agreed unanimously by stockbrokers and financial analysts, the different types of investments are as follows:

- Short-term investments: Short-term investments are investments anywhere between 1 year to 3 years. Any investment for less than 1 year can be defined as ultra-short investments.

- Long-Term Investments: Investment horizon of more than 5 years should ideally come under Long-Term Investments.

- Medium Term Investments: Medium Term Investments are investments for a period between 3 years to 5 years.

Why Long-Term Investments?

It was Friedrich Nietzsche who said, “He who has a why to live can bear almost any how”. This also applies to long-term investments. When you have incisive clarity about the intrinsic value of the share, in-depth knowledge of the fundamentals of the company and have clearly devised financial goals, the temporal peaks and troughs don’t affect you, though you’re intricately aware of the market. Logic always supersedes emotions. You avoid being a victim to falsified rumours, and fraudulent claims. You remain calm, patient and stay invested while all hell breaks loose around you. As the legendary investor Warren Buffet says “The stock market is a device for transferring money from the impatient to the patient”.

There are two expressions often running in tandem but conflicting with one another “follow your dreams” and “follow the crowd”. If you follow your dreams, you require extensive financial planning which requires allocating money to long-term investments so you can fulfil your big-budgeted, long-cherished dreams of vacationing in Hawaii, having a grand wedding of your children, possessing a corpus of funds for higher education, etc. The best way to fulfil your dreams is to stay the course, with a long-term vision; remain invested in the financial instruments till it reaches its highest perceived value or till the investment value is enormous enough to fulfil your long-held dreams.

Now when you take the other expression “follow the crowd”. You may put your dreams in the backburner and get swayed by the short-term volatile movement, which is often a reflection of investors’ paranoia or irrational optimism. In such a scenario, you’ll either cash in and make a profit or sell the stocks off and record a loss. In both cases, your dreams remain unfulfilled. So, while others revel in pleasure over few sultry gains and others sob profusely in sorrow over trivial losses, you stay invested while the paltry sum in thousands invested by you in some distant past slowly burgeons into an immense fortune worth in millions.

And then onlookers credits luck for the glory, wealth and even fame while you acutely know it was patience, tenacity, the initial drudgery doing extensive research, faith in your expert and more importantly LONG-TERM INVESTMENTS that brought the envious success and stunning victory.

It is also essential to consider that courtesy, widespread advancements in medicine; people are living longer and healthier lives. However, merely entrusting your money into the safe hands of the bank will not grow your money much and may not ensure a stress-free, relaxing retirement. Hence, given the volatile conditions of the market, the teetering global economy, and the vulnerability of the world to shocks and events beyond its control, long-term investments for a stable future seems to be a wise decision.

Hence, its Long-term investments that will fulfil your investment goals so you can live a life you have always dreamed of.

watch our video to learn about long term investing

Recipe for Successful Long-Term Investing:

If you’re for the long haul, please make sure that you take care of these fundamental ingredients required for creating the recipe of long-term successful investing:

“Compound interest is the eighth wonder of the world. He who understands it earns it; he who doesn’t, pays it” quoted by Albert Einstein. Compound interest can be defined as the interest accumulated on the initial principal and also on the accumulated earnings or interests of the previous periods. Compounding takes place when the interest or gains on initial investment is added back to the principal amount to calculate the returns for the subsequent period. Let us understand the power of compounding.

Let us take two people Mukesh and Anil.

Mukesh and Anil both made long-term investments worth Rs 2,00,000. Both opt for interest to be calculated as compound interest. However, Mukesh’s age at the time of investing was 25 years while Anil’s age was 30 years. Both stay invested until the age of 60. Let us calculate the difference between Mukesh’s returns and Anil’s returns from their long-term investments, for a mere difference of 5 years

| Particulars | Mukesh | Anil |

| Principal Invested | 2,00,000 | 2,00,000 |

| Rate of Interest | 20% | 20% |

| Age at the time of Investing | 25 | 30 |

| Age at Maturity | 60 | 60 |

| Amount at maturity (in Rs) | ₹ 11,81,33,646 | ₹ 4,74,75,263 |

| Difference in final value (in Rs) | ₹ 7,06,58,383 |

Now let us understand how much more Mukesh earned from his long-term investments for a difference in investment duration amounting to 5 years.

He earned a colossal corpus of Rs 7,06,58,383 more than Anil. That means he made 1.49X times the amount Anil receives, from his long-term investments.

He makes 149% more than Anil for merely investing for 16.67% more time than Anil.

Let that sink in.

This is the genuine power of compounding.

Hence, the magic ingredient/elixir/ambrosia that makes compounding work is time.

Essentially, it creates a chain reaction by generating returns upon returns until you stay invested in the financial instrument, which makes your wealth slowly snowball into a fortune. Hence, the longer you stay invested in your long-term investments, the more time you give your interest income to compound and grow. So, it is never too early to start investing as the sooner you invest, the sooner you allow your returns to generate further returns until you stay invested.

Spread your eggs among different baskets.

The world is riddled with uncertainty. You must understand that despite the innumerable forecasts, the best analysis, the world has always thrown down the gauntlet to defy the best of us. Hence, as a long-term investor, it is imperative to mitigate the investment risks by diversifying the portfolio in different asset classes, in diverse geographical regions, etc. Let us understand diversification and importance of it through the example of a fruit vendor. As a fruit vendor, you’d want to sell a variety of fruits instead of just one, so if a large unforeseen event like a hurricane brings Maharashtra to a standstill, completely cutting off supplies of oranges from Nagpur and bananas from Nashik, you can sell the apples from Himachal Pradesh or guavas from Prayagraj in Uttar Pradesh.

Similarly, you can benefit from having strawberries in your fruits catalogue in winter due to their seasonal demand. Think of the fruits as different styles, sectors, regions, by having a diversified portfolio; you mitigate the risk of losing all money at once. At the same time, you’re spreading your risk among a host of financial instruments from different geographies and sectors; so in case of an unforeseen event, the losses suffered by one investment are mitigated or offset by the profits earned in other investments. Also, you don’t want to lose on gains made in other asset classes during their bull run, just like strawberries in winter in the example.

Ride the Winner

If some of your holdings in long-term investments are doing exceptionally well, there is always this temptation to cash in and make a profit. If you bought 100 shares of Page Industries at Rs 1500 in Jan 2011, and you witness the uninhibited rise in the share prices and see the prices touching Rs 3500 in Jan 2013, you’ll be naturally lured into selling the shares and booking a profit of a whopping Rs 2000 per share, i.e. Rs 20,00,000 in total. However, if you hold your horses and continue holding the stocks you would see the price of the share reaching a mammoth of Rs 36000 in Aug 2018, even now the shares are trading at Rs19000, that is still an appreciation of 1300%. If you’re in the game for the long run, you want your long-term investments to grow and reach their fullest potential, so when you find the winners, hold them and cherish them. Peter Lynch famously spoke about “ten baggers” – the stocks that have the potential to grow tenfold. He attributed his success to such a handful of stocks in his portfolio. However, this requires unyielding discipline to hold on to the stocks even after their prices have exponentially risen and increased by many multiples if you think there is upside potential. You overcome the initial euphoria of your investments riding the bull run and let cold, unyielding investment logic take over. You consider each of the long-term investments on its own merits, keep emotional biases at bay, hold on to those long-term investments which are yet to achieve its zenith irrespective of the considerable gains you may earn presently by selling the shares.

Relinquish the Loser

There is always this engulfing temptation to hold on to poorly performing stocks with the false hopes that it may rebound in the future or worse still to increase your holdings at a lower price. When the housing bubble burst in 2007, when the stocks prices were crumbling down at an unprecedented pace, the investors stiffened and froze. Many did not react until the value of the portfolio got brutally truncated to 40-50% of the portfolio value. During the 2008 financial crisis, many opined “I’ll wait till the stocks reach their original price and then sell off. Then at least I’ll break-even”. First of all, there is no guarantee that a stock may rebound after a protracted, lengthy decline. Also, many investors assume that if the price of shares reduces by 20%, the price needs to simply increase by 20%, which is a fallacious assumption, as described in the chart below.

| Percentage Loss | Percentage Rise to Break Even |

| 10% | 11% |

| 15% | 18% |

| 20% | 25% |

| 30% | 43% |

| 40% | 67% |

| 50% | 100% |

So if your stock worth Rs 1000 is reduced by 20%, i.e. 200, to Rs 800, it has to rise by 25% to reach the price of Rs 1000. Even though acknowledging losing stocks may seem to be a crushing failure, it is imperative to sell the shares and take a few lusty blows to the ego, and stem further loss rather than holding on to the stocks for emotional reasons, defying investment logic and taking a gigantic loss in the future. There is no shame in accepting mistakes and relinquishing the shares eroding in value with no foreseeable recovery and extracting valuable lessons from them.

Do not try timing the market.

Let’s suppose you invested Rs 42000 to purchase 500 shares of the company Rana holdings in 2008 when the world suffered the worst global financial crisis since the Great Depression in the 1930s; you would be endowed with an enormous wealth of Rs 1.24 crores. This was the time when investors were paranoid of a Financial Apocalypse and were selling their investments off at deep bottom prices. Do you know there were 152 companies listed in the NSE that have recorded in its annals a whopping 1000% to 30000% growth since the 2008 Global financial crisis? Investors always have this overbearing impulse to get in when the markets are doing exceptionally good and get out when the needle of the market is pointing down, but this leads to the investors getting entrapped in fear of missing out and putting their money in the markets when it’s most expensive and exiting the markets when the prices are low, when it is apt to increase the holdings at a lower price to profiteer from the prices rising in the future.

Re-invest dividends

Let us revisit the concept of compounding in Benjamin Franklin’s words “Money makes money. And the money that money makes, makes money”. Re-invest dividends and harness the power of compounding. The compounding effect can significantly increase the returns if the same dividends are reinvested in equity over time. Significant growth in a portfolio at times comes from reinvested dividends rather than appreciation in stock figures. A meagre, inconsequential income will metamorphose into a fortune over time. Choose stocks with a solid history of dividends, reinvest those dividends, and earn sizable returns on your long-term investments.

Do not let Volatility Derail you

Volatility is normal – a market life cycle comprising peaks and troughs characterizes a gamut of industries including the financial market. There are going to be severe drawdowns in the market from time to time. It is unheard of any stock only to move upwards. However, when flagrant or obscure signals start to indicate tumultuous times ahead, it pays to stay invested. When you are aiming for successful long-term investing, occasional peaks and troughs are inconsequential, the market prices, at times, are not a pure reflection of the future potential of the stock. Sometimes, it reflects investors’ exaggerated paranoia or palpable excitement. A long-term investor should steer clear of it and should focus mainly on the fundamentals of the company, future growth trajectory buoyed by the long-term stability of the market. Looking at previous drawdowns, the length of the bear markets has always been less than that of subsequent bull runs with any losses suffered during the bear market reversed during the tottering bull runs. Troubled times aren’t a sign to sell everything.

Find expert help

Stocks are usually preferred as long-term investments. But investing in stocks is an arduous and tumultuous journey. It requires extensive analysis of the company and the overall market. It involves various steps from listing the companies, examining the fundamentals of the company, predicting the future growth trajectory of the company, identifying the competitors, forecasting future challenges, and in the end, having a broad market outlook. It also requires extensive calculations such as Price/Equities Ratio, etc. which a layman investor is oblivious to. Investing can be extremely time-consuming, and a layman investor overburdened with responsibilities and assailed with an inescapable amount of work will often find it challenging to find the time and invest in stocks. In such a scenario, we have platforms like StockBasket, where you can invest in expert-selected stocks or a great mini portfolio to build long term wealth or make long-term investments. You have access to a plethora of baskets, which is nothing but a pool of shares, where shares are handpicked to match your diverse financial goals. Also, the baskets are carefully monitored and rebalanced on a timely basis. Stock Basket has generated explosive returns of over 800% since its inception in 2007.

The stock market is replete with examples where a tiny amount slowly snowballs into a fortune catching the investors off-guard.

E.g. Rs 10000 invested in the stock of an IT company Infosys in June 1993 would pay Rs 2.97 crores in Dec 2017

Rs 10000 invested in Eicher Motors in January 1990, would have been 2.01 crores in Dec 2017

Here a measly amount of Rs 10000 begets a colossal treasure of money worth in crores, Hence, Long-Term investments endeavours to create a massive trove of wealth while other investments seek to preserve wealth. We must reinstate the tried and tested principles and reinforce the critical habits of successful investors. Platforms like StockBasket with its carefully curated portfolio can provide you with a launchpad to journey towards long-term investments, help accomplish a range of financial goals and ensure success in all areas of life.

We believe that patience, poise, a combination of the timeless investing principles, sound financial advice, and deeper insights can help every investor score many wins enough to turn every captivating dream into a tangible reality.

1 Comment

The knowledge receive is unbelievable. Waiting for another writing.